Network costs, regulatory timing, and voyage security are the dominant levers right now. New bilateral port fees are changing route economics in real time, policy indecision on carbon pricing is pushing investment choices to the right, and enforcement or incidents along critical corridors are adding delay and insurance friction. The result is tighter utilization in select trades and a more cautious approach to contracts and coverage.

Top Developments Impacting Maritime P&L - 10/20/25

Story

Summary

Business Mechanics

Bottom-Line Effect

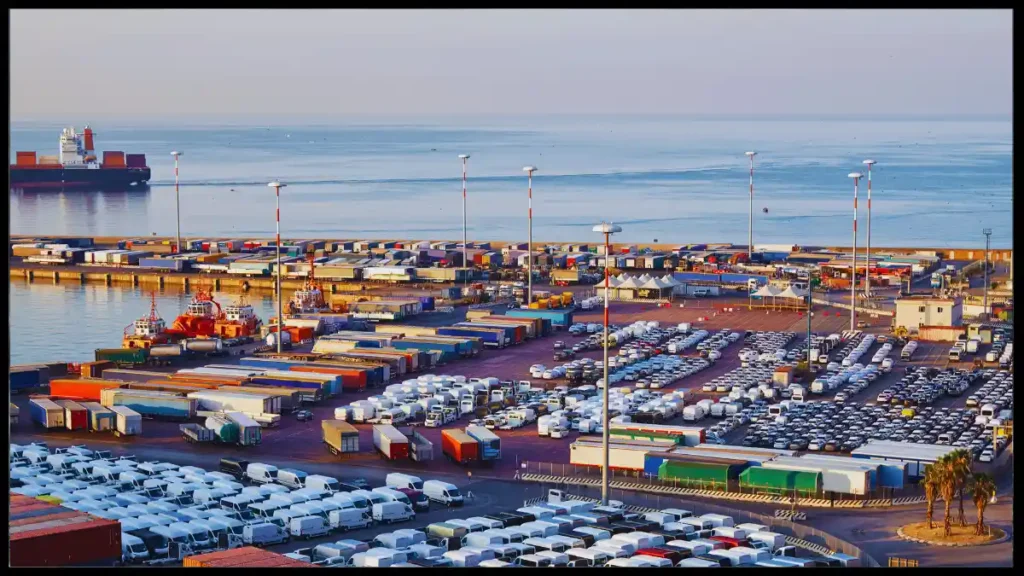

U.S.–China special port fees begin

Per-call charges apply on both sides, and carriers respond with rerouting and selective blank sailings.

Fee exposure informs port rotation choices, surcharges move through contracts, network buffers shrink.

📈 Tighter capacity supports spot rates and TCEs on affected lanes, 📉 higher per-call costs for exposed trades.

IMO postpones global carbon pricing decision

A one-year delay keeps the sector cost curve uncertain and slows some fuel and retrofit programs.

Charter parties add stronger change-of-law and emissions clauses, lenders widen risk premia until policy is clearer.

Longer fixture cycles; detention/diversion risk for opaque hulls

Gulf of Aden / Bab el-Mandeb transits

Security incident; elevated war-risk pricing

Convoying/diversions; added time and bunkers; schedule slippage

Atlantic Basin → India crude options

Substitution interest; terminal congestion risk

Longer hauls for Aframax/Suezmax; demurrage sensitivity at peaks

Clause & Coverage Pack

Change-of-law / sanctions warranties aligned to current fee and inspection regimes

Proof-of-origin and attestation stack for refined-product trades into Europe

AIS continuity and ownership/manager verification for hull screening

War-risk, additional premium triggers, and security routing language for high-risk corridors

Carbon-cost pass-through riders pending global levy timing

Delay & Insurance Impact Estimator

$0 delay

$0 compliance

$0 total

$0.00 per unit

Quick Watchboard

Port-call patterns and surcharge adoption on affected U.S.–China rotations

Inspection/boarding posture for shadow-fleet corridors and related hull lists

Security advisories and routing choices around Bab el-Mandeb

Clause updates from clubs, lenders, and major charterers on carbon and sanctions

Orderbook changes and delivery schedules that shape 2027–2029 capacity

These elements focus on where earnings are made or lost: fee pass-through, inspection-driven delay and insurance friction, and corridor-specific routing choices. The calculators let you approximate voyage-level impacts under different fee and risk assumptions, while the heatboard and clause pack highlight where operational discipline and contract language protect margins in the current environment.