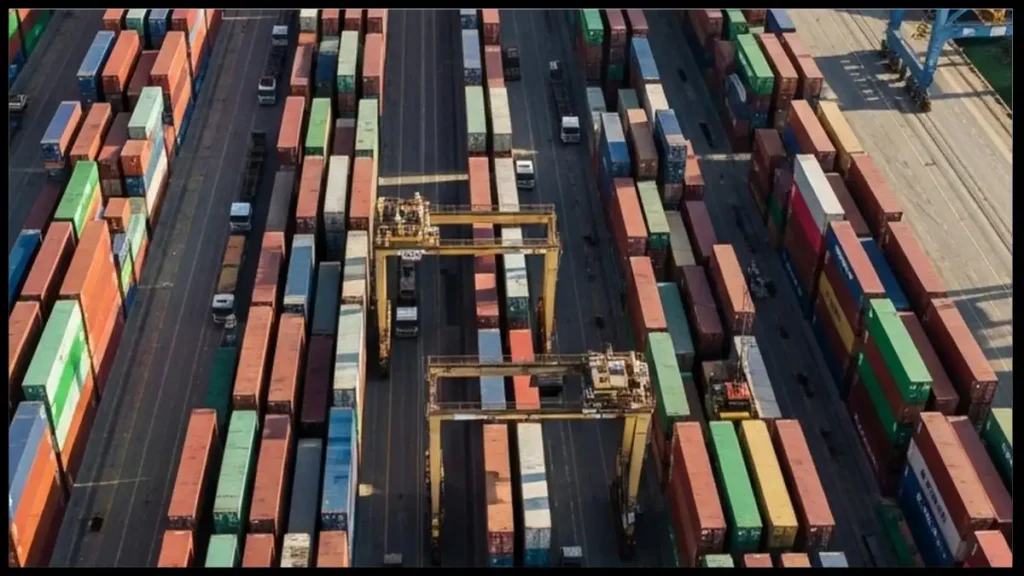

Despite trade tensions and policy noise, China’s box volumes are still climbing. Shanghai has crossed the 50 million TEU mark for 2025 a month earlier than last year, while Ningbo-Zhoushan has passed 40 million TEU for the first time, putting the two port complexes above 90 million TEU combined in just 11 months.

Click here for 30 second China port summary

Shanghai and Ningbo-Zhoushan in one quick read

Shanghai has crossed the 50 million TEU mark for the year ahead of last year’s pace and Ningbo-Zhoushan has passed 40 million TEU for the first time, putting the two ports above 90 million TEU combined with time still left in the calendar. That confirms East China’s role as a central load engine for global container trades and sets the tone for capacity planning, box positioning and inland logistics into the next cycle.

Demand signal – High and still rising volumes at Shanghai and Ningbo-Zhoushan support the view that core export and import flows through East China remain strong, even when spot indices are choppy.

Network and equipment – Mainline and feeder loops are likely to lean even harder on these hubs, which affects where the biggest ships are deployed, how often they call and how quickly empties are turned and repositioned.

Cost and resilience – Concentrating more cargo through a few mega gateways raises the premium on reliable hinterland corridors, depot stock management and contingency routing, because any local disruption can ripple quickly into schedule gaps and extra costs.

Bottom line

The 90 million TEU milestone is a supportive backdrop for carrier utilisation and investment plans, but it also narrows the margin for error. Lines, forwarders and cargo owners that adjust networks, box strategies and inland capacity around Shanghai and Ningbo-Zhoushan are better positioned to turn today’s throughput strength into stable earnings rather than congestion-driven volatility.

Shanghai and Ningbo-Zhoushan cross 90M TEU combined in 2025

Item

Summary

Business mechanics

Bottom-line effect

Record headline volumes

Shanghai has passed 50 million TEU for 2025 about a month earlier than last year, while Ningbo-Zhoushan has handled 40 million TEU for the first time, taking the pair beyond 90 million TEU with one month still to count.

Sustained high volumes into year end are a demand signal for mainline and feeder capacity planning. Carriers and box owners read this as support for network utilisation even if freight indices flatten or soften in the short term.

📈 Underpins earnings visibility for services tied to East China load ports and keeps high utilisation in view on core headhaul trades. 📉 Leaves less slack in the system when disruptions hit, which can inflate costs when schedules slip.

Shanghai throughput and automation

Shanghai has kept its position as the top global container port for 16 years and is averaging more than 4 million TEU a month. Growth now leans on automation and integrated operations rather than just new quay length.

Remote-controlled cranes, unmanned yard vehicles, AI-driven planning tools and an integrated control system allow tighter berth windows and faster turnarounds, which helps carriers hold schedule integrity at very high volume levels.

📈 High productivity at the world’s largest container hub supports faster port stays and protects box rotation. 📉 Operators that do not match these efficiency gains on other legs may see imbalance in schedule and equipment flows.

Ningbo-Zhoushan growth and scale

Ningbo-Zhoushan has stepped up from 39.3 million TEU in 2024 to 40 million TEU reached by early December, with growth accelerating as the port moves from 30 to 40 million TEU in four years instead of six.

The complex is linked to more than 300 routes serving 600 ports in 200 countries and regions, supported by over 210 deepsea berths. This strengthens its role as a parallel gateway to Shanghai for both mainline calls and feeders.

📈 More capacity and connectivity in East China gives carriers extra options for pairing loops and transhipment. 📉 Strong pull into these hubs can disadvantage secondary ports that may see thinner calls and weaker box availability.

Network planning and equipment flows

High and rising moves at these hubs anchor east-west and regional schedules, influencing where carriers base their biggest ships, where feeders connect, and how quickly empties are repositioned out of China.

Lines may cluster more loops around Shanghai and Ningbo-Zhoushan, using them as consolidation points for inland and coastal cargo. This can tighten equipment availability in nearby regions if imbalances are not actively managed.

📈 Stronger hub status can support better slot utilisation and box turns for operators that align networks with these flows. 📉 Smaller shippers and outport origins may pay more for equipment or face longer lead times when boxes are scarce.

Hinterland links and congestion risk

Rail, barge and truck corridors feeding Shanghai and Ningbo-Zhoushan are carrying more volume and will be the first place where any policy, weather or infrastructure shocks show up as delays.

Even if quay-side operations are efficient, inland bottlenecks can slow box evacuation and build yard density. Localised congestion can then ripple into schedule gaps, missed connections and rolled boxes.

📉 Extra dwell time and rerouting inland legs increase logistics cost per box and working capital needs. 📈 Forwarders and BCOs that secure reliable hinterland capacity can lock in more stable service levels at busy gateways.

Outlook for carriers and owners

Record levels at two core gateways suggest that, while policy risk and demand swings remain, the underlying container flow out of China is still strong enough to support large mainline fleets and ongoing investment in bigger ships and terminals.

For owners, high throughput at key ports reinforces the case for large, efficient tonnage on mainline services and nimble feeder tonnage around them, provided fleets remain flexible enough to pivot if trade patterns shift.

📈 Healthy core demand supports utilisation assumptions in many container fleet plans and financing models. 📉 Over-ordering or concentrating too much exposure on a narrow set of China-centric trades still leaves earnings vulnerable if policy or demand turns.

Notes: Summary based on reported 2025 throughput milestones at the ports of Shanghai and Ningbo-Zhoushan, including Shanghai surpassing 50 million TEU by late November and Ningbo-Zhoushan reaching 40 million TEU on December 2. Actual effects vary by service, contract structure, inland routing and equipment strategy.

East China container pulse behind the 90M TEU headline

Quick visual read on how Shanghai and Ningbo-Zhoushan are shaping network loads, with a lens on volume, growth pace and hub gravity.

Throughput and growth direction (illustrative)

Port / combo

2025 run-rate

Versus last year

Directional bar

Shanghai

50M+ TEU already cleared

Earlier crossing of 50M mark

High, steady uplift

Ningbo-Zhoushan

40M+ TEU for the first time

Faster step from 30M to 40M

Strong acceleration

Combined

90M+ TEU across 11 months

New bar for gateway pair

Very elevated hub load

Bars are qualitative and show direction, not exact percentages. Actual performance depends on final full year counts and trade mix.

Tailwinds and watch points for container stakeholders

Tailwinds for carriers and terminals

Watch points for costs and resilience

High, durable flows into Shanghai and Ningbo-Zhoushan support utilisation assumptions for mainline and feeder networks.

Automation and integrated planning at the big hubs help protect berth productivity and box rotation at heavy load.

Stable volume underpins the business case for ongoing investments in larger ships, hub upgrades and digital tools.

More volume through a few mega hubs increases sensitivity to localised disruption in terminals or hinterland corridors.

Secondary ports risk thinner calls and scarcer equipment, which can push up inland and feeder costs for some shippers.

Network misalignment elsewhere can still erase gains if vessels lose time at less efficient ports on the same loop.

Network planning lens: questions for the commercial desk

Question

What to check

Why it matters

Are loops aligned with new load centres?

Port pairs, call frequency and cut-off times at Shanghai and Ningbo-Zhoushan versus nearby alternatives.

Misaligned loops can suffer rolled boxes and weaker schedule integrity even in a strong demand environment.

Is equipment balancing keeping up?

Empty flows out of China, turn times, and depot stock levels in nearby regions and key outports.

Poor box positioning can turn a volume tailwind into higher costs and service variability for customers.

How exposed are you to hinterland bottlenecks?

Rail, barge and trucking capacity on main corridors into and out of the two hubs, including peak season stress points.

Gate and inland constraints can drag down performance even where quay-side productivity is high.

This lens is intended for carrier, NVO and BCO planning teams using Shanghai and Ningbo-Zhoushan as core East China gateways.

For container lines, box owners and cargo interests, Shanghai and Ningbo-Zhoushan pushing past 90 million TEU together is more than a record headline. It confirms that East China remains the central load engine for many global networks, supporting utilisation and investment plans even as freight indices move around. At the same time, concentrating so much volume through a small number of mega hubs raises the premium on robust inland links, equipment management and contingency routing. Those who treat these two gateways as the anchor points in a broader, flexible network are better placed to turn today’s throughput strength into sustainable earnings instead of fragile, congestion-sensitive margins.