HomeCapital’s $770m LNG Newbuild Bet with Three High-Spec Ships Timed for the 2028–2029 Tight Window

Capital’s $770m LNG Newbuild Bet with Three High-Spec Ships Timed for the 2028–2029 Tight Window

December 30, 2025

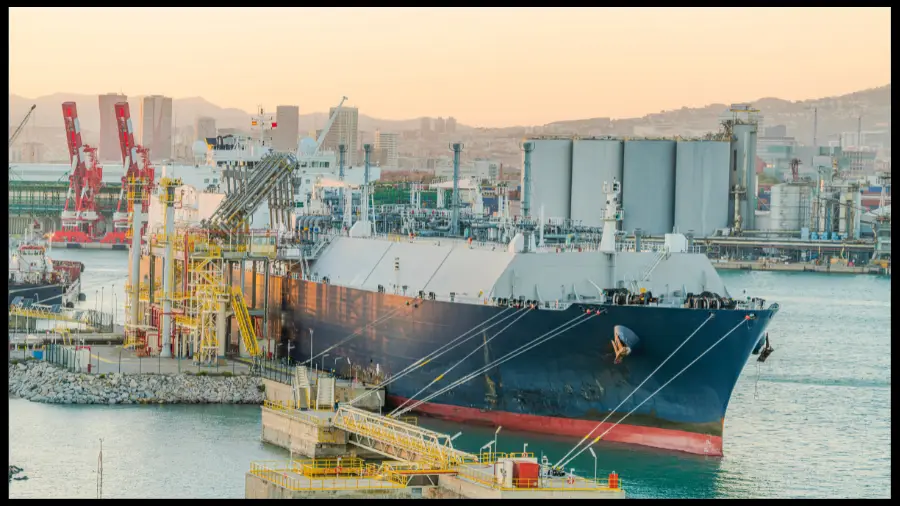

Capital Clean Energy Carriers (CCEC) has ordered three new LNG carriers at HD Hyundai Samho in South Korea for an en-bloc shipbuilding price of $769.5 million (about $770 million). Deliveries are scheduled for the third quarter of 2028 (one ship) and the first quarter of 2029 (two ships). The company says the designs include specification upgrades intended to rank among the most efficient LNG carriers globally on fuel consumption and boil-off, and that the delivery window lines up with expected growth in LNG supply and shipping demand later this decade.

Capital books three LNG newbuilds for a late-decade delivery window

Capital Clean Energy Carriers has ordered three LNG carriers at HD Hyundai Samho for an en-bloc shipbuilding price of $769.5 million. Delivery is scheduled for one ship in Q3 2028 and two ships in Q1 2029, with the company highlighting specification upgrades aimed at top-tier fuel consumption and boil-off performance.

The hard facts

3 ships, $769.5m total. Delivery timing: 1 in Q3 2028 and 2 in Q1 2029. Yard: HD Hyundai Samho.

The positioning

The order targets the 2028 to 2029 demand window that many LNG market participants associate with higher seaborne volumes as new supply ramps up, while leaning into efficiency as a commercial differentiator.

The cash and coverage frame

CCEC cites about $3.0bn of contracted revenue and 6.9 years average remaining charter duration, and disclosed $386.1m of advance payments made to shipyards for its under-construction fleet as of Dec 29, 2025.

Bottom line

This is a deliberate bet on late-decade LNG shipping tightness, backed by a higher-spec build narrative and a contracted revenue base, with the main swing factors being delivery execution and where LNG project ramp-ups land versus the 2028 to 2029 handover dates.

Capital Clean Energy Carriers orders three LNG carriers for $769.5m, delivering in 2028 to 2029

Item

Summary

Business mechanics

Bottom-line effect

Order headline

CCEC ordered three latest-technology LNG carriers at HD Hyundai Samho in South Korea for an en-bloc shipbuilding price of $769.5 million.

A three-ship block secures yard slots in one decision and simplifies specification standardization, spares planning, and future commercial marketing versus a one-off build.

📈 Adds scale in a premium asset class and supports fleet “scarcity value” claims. 📉 Raises committed capex and increases exposure to shipyard delivery and financing conditions.

Delivery timing

One vessel is scheduled for delivery in the third quarter of 2028, with two more scheduled for the first quarter of 2029.

Deliveries clustered late decade can be positioned for charterers planning coverage against new LNG supply ramp-ups, but they also concentrate execution risk if market conditions shift.

📈 If late-decade demand tightens as expected, these ships arrive when modern tonnage can price well. 📉 If the cycle softens, late deliveries can face tougher charter negotiations.

Efficiency angle

CCEC says the ships include specification upgrades and are expected to rank among the most efficient LNG carriers globally in fuel consumption and boil-off rates.

In LNG shipping, small differences in fuel use and boil-off translate into measurable voyage economics and cargo delivery outcomes, which can influence charter attractiveness and duration.

📈 Better economics can support stronger time charter pricing and utilization. 📉 “Top-tier” specs usually cost more upfront, so payback depends on charter terms and market spreads.

Fleet scale and pipeline

CCEC says it has 12 LNG carriers on the water and nine LNG carriers on order after this deal, with LNG newbuilding deliveries spanning from the third quarter of 2026 through the first quarter of 2029.

A visible delivery pipeline can strengthen chartering conversations with buyers who want multi-vessel coverage over multiple years, but it also increases management workload on construction supervision and pre-delivery commercialization.

📈 Larger platform can win bundled charters and repeat business. 📉 Concentrated fleet growth increases sensitivity to LNG shipping cycle shifts and any construction delays.

Commercial cover

CCEC reports about $3.0 billion of contracted revenue and an average remaining charter duration of 6.9 years, and says it secured long-term employment in 2025 for three LNG newbuildings.

Long-duration charter cover cushions cash flow while leaving some capacity open for upside. The mix matters because contracted ships stabilize earnings while open ships carry cycle exposure.

📈 Higher earnings visibility helps funding and dividend planning. 📉 Too much open exposure can amplify volatility if spot and short-term rates weaken.

Capex and payments

CCEC revised its capex schedule after contracting these ships and said it had paid $386.1 million in advance to shipyards toward its under-construction fleet as of December 29, 2025.

Advance payments and milestone profiles determine liquidity needs well before delivery. The company also described recycling capital from its legacy container fleet as part of its balance-sheet approach.

📈 Clear capex roadmap supports financing conversations and investor expectations. 📉 Pre-delivery cash commitments raise the cost of any schedule slippage or market downturn.

Market timing thesis

CCEC linked the delivery window to expected LNG supply growth, citing forecasts that global LNG liquefaction capacity could rise from about 493 mtpa today to at least 649 mtpa by 2030.

More liquefaction capacity typically expands seaborne LNG volumes and ton-mile demand, but the timing depends on project start-ups, utilization rates, and destination market pull.

📈 If project ramp-ups track the forecast curve, shipping demand can tighten into late decade. 📉 Delays in LNG projects or weaker demand can push the tightness further out.

Notes: Figures and dates are drawn from CCEC’s December 29, 2025 release and market reporting, including: $769.5m en-bloc price, delivery schedule (Q3 2028 and Q1 2029), fleet counts (12 LNG carriers in the water, nine on order), contracted revenue (~$3.0bn), average remaining charter duration (6.9 years), and advance shipyard payments ($386.1m). LNG liquefaction capacity figures are presented as the company’s cited forecast and can change with project timelines.

What this order really signals: late-decade capacity positioning and cash-visibility math

The headline is three ships. The subtext is timing, efficiency positioning, and how much of the LNG cycle an owner wants on contract versus exposed to the market when those deliveries arrive.

Numbers that frame the economics

Derived from disclosed figures

Approx. build cost per ship

~$256.5m

$769.5m en-bloc divided by 3 ships.

Delivery clustering

1 in Q3 2028

2 in Q1 2029, concentrating market exposure into one window.

Balance-sheet signal

$386.1m

Advance payments reported as already made to yards across the under-construction program.

Earnings-visibility anchor

~$3.0bn

Contracted revenue base cited, with 6.9 years average remaining charter duration.

Late-decade timing, explained

Why 2028 to 2029 slots matter

LNG shipping demand tends to tighten in waves when new supply ramps up. Deliveries landing close together can either look well-timed if employment demand rises, or feel concentrated if chartering appetite softens at the wrong moment.

The reality of “schedule risk”

Build programs are paid for well before earnings start. If delivery dates slip, the cost is usually not just time, but also how charter cover and financing expectations line up with the final handover month.

Timeline snapshot

Q3 2028

1 LNG carrier delivery

Q1 2029

2 LNG carrier deliveries

Efficiency claims, translated to shipping outcomes

Fuel consumption and boil-off

For LNG carriers, better fuel efficiency and lower boil-off typically mean improved voyage economics and stronger commercial appeal to charterers focused on delivered energy value and emissions performance.

Where “premium spec” pays back

Premium specifications tend to matter most on longer routes and tighter schedules, where incremental savings compound, and where charterers compare fleets on efficiency, availability, and operational consistency.

The trade-off

Higher-spec ships usually have higher capex. The commercial impact is tied to how much of the benefit is captured in charter terms and utilization when the vessels enter service.

Who feels this order first

Charterers

More late-decade, high-spec availability becomes part of multi-year coverage planning, especially for buyers who prefer standardized modern tonnage.

Shipyards and suppliers

A three-ship block reinforces slot demand at a specific yard and supports longer procurement runs for equipment and systems tied to a standardized design.

Financiers and investors

The focus shifts to payment milestones, liquidity runway, and how the contracted revenue base offsets the pre-delivery cash profile.

Competing owners

Additional modern deliveries increase the pool of efficient ships late decade, which can widen performance differences between newer and older LNG tonnage.

Capital Clean Energy Carriers’ three-ship, $769.5 million LNG newbuilding order is a late-decade positioning move that pairs a concentrated 2028 to 2029 delivery schedule with an efficiency-forward specification pitch. The commercial significance sits in how those ships land relative to LNG supply ramp-ups and charter coverage demand, while the financial significance sits in the pre-delivery payment curve and the extent to which existing contracted revenue and charter duration help buffer construction-period cash commitments.