HomeRisk Premium Rising: IUMI Signals a New Cost Curve for Shipping

Risk Premium Rising: IUMI Signals a New Cost Curve for Shipping

September 8, 2025

ShipUniverse Weekly

Get the maritime stories operators are watching.

Stay ahead of vessel markets, port disruption, maritime technology, and more.

Subscribe to the NewsletterFree weekly maritime insights for owners, operators, brokers, suppliers, and decision makers.

At IUMI’s Singapore conference, President Frédéric Denèfle warned that trade fragmentation and geopolitical shocks are reshaping marine underwriting, pushing premiums up, tightening terms, and forcing operators to treat insurance as a strategic lever rather than a background bill. Singapore officials also framed marine insurance as a “strategic enabler” for trade resiliency. Below is a practical readout of what’s changing and how it hits budgets.

Marine Insurance Shifts Highlighted at IUMI Singapore

Theme

What’s Changing & Who’s Affected

Mechanics

Bottom-Line Effect

Fragmented Trade

Insurers price a world that’s less seamless: more regional routes, diversion around conflict zones, and different rulebooks. Owners with cross-theatre exposure feel it first.

Higher risk loads on corridors near flashpoints (e.g., Red Sea spillovers); accumulation limits tightened at key hubs.

📉 Premium creep and deductibles up on exposed lanes; 📈 incentive to optimize routing and port calls.

Tighter Policy Terms

Underwriters push for clearer voyage declarations, sanctions checks, and cargo disclosures. Managers and charterers face heavier admin.

Stricter warranties; exclusions clarified; documentation/ITP (information to principals) expanded.

📉 Higher compliance overhead; ↔ improved claim certainty if documentation is robust.

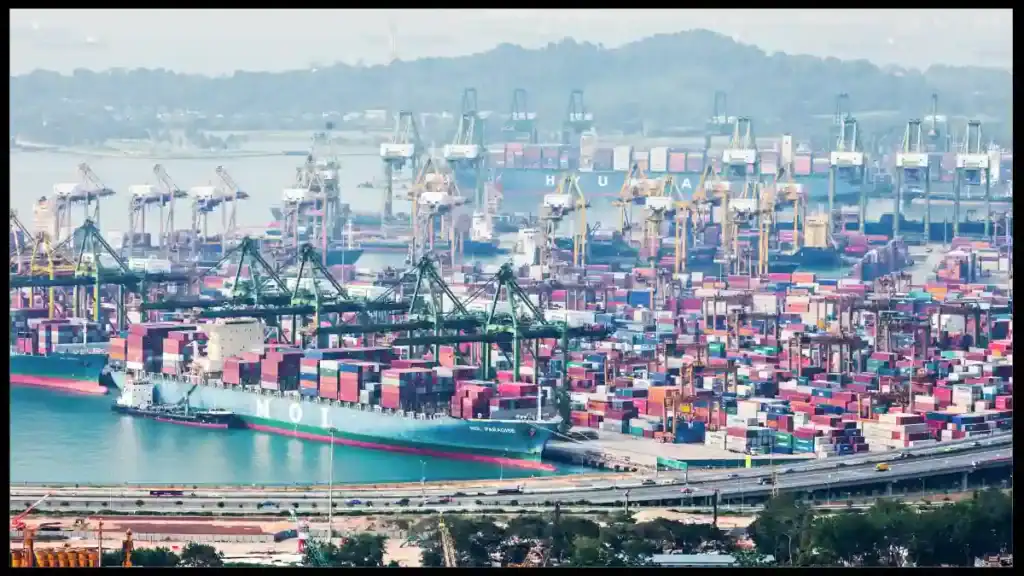

Port & Cargo Accumulation

Mega-ports and ultra-large vessels concentrate values. Cargo policies see more scrutiny on stock throughput and aggregation.

Revised aggregation models, sub-limits for storage peaks, higher catastrophe loads.

📉 Potential rate/limit pressure for large inventory positions; 📈 savings if inventory smoothing reduces peak exposure.

Fuel Transition Risk

As fleets trial new fuels and retrofits, hull/machinery underwriting wants evidence on safety and operations.

Data-driven maintenance regimes and trials reduce perceived technical risk.

↔ Neutral to 📈 if operators can demonstrate controls—potentially better terms versus late adopters.

Cost Inflation in Claims

Higher repair costs, parts scarcity, and longer yard queues lift average claim severity across hull and cargo.

Repair day-rates up; OEM lead times extend; salvage/logistics priced higher in conflict-adjacent waters.

📉 Premiums trend up to match loss costs; 📉 longer off-hire risk if yard slots are tight.

Insurance as Enabler

Policy design and certainty of cover become a planning input, not an afterthought, especially for ports and national trade programs.

Early engagement with underwriters on routes, security measures, and data sharing.

📈 Better pricing/availability for prepared operators; 📉 penalties for late or opaque submissions.

Note: Drawn from IUMI Singapore briefings and coverage on geopolitical fragmentation, risk concentration, and underwriting shifts; marine insurance framed by Singapore as a trade enabler.

📈 Winners

📉 Losers

Insurers with disciplined underwriting: ability to price corridor-specific risks and tighten terms supports margin quality.

Owners with robust compliance & data: strong sanctions screening, route disclosures, and maintenance data can win better rates/terms.

Ports investing in risk controls: improved security, inventory smoothing, and resilience planning lower aggregation exposures.

Banks & brokers specializing in complex risk: higher demand for structuring cover, captives, and multi-jurisdiction clauses.

Operators on lower-risk corridors: relative cost advantage as premiums climb faster on conflict-adjacent routes.

Cross-theatre fleets without clear declarations: opaque routing/documentation face higher premiums, deductibles, and exclusions.

Trades near flashpoints or sanction exposure: cargo/hull cover becomes costlier; some risks may be partially uninsurable.

Operators relying on just-in-time inventory: accumulation limits and stock throughput scrutiny raise costs at mega-hubs.

Late adopters of fuel/retrofit safety protocols: uncertainty around alternative fuels elevates H&M pricing and survey burdens.

Thin-margin charterers on fixed rates: limited ability to pass premium creep through to customers compresses earnings.

Note: Directional view based on IUMI conference commentary and corroborating maritime insurance coverage.

Shifting Risk Lines: Insurance Is Steering More of Our Decisions

At IUMI Singapore the tone was clear: marine insurance is no longer a back-office cost, it’s becoming a strategic lever. We’ve been reflecting on how this reframes decisions for owners, ports, and financiers:

Risk is now priced corridor by corridor, forcing owners to be more selective about routes.

Data discipline is rewarded, with better terms for those who can prove maintenance and compliance.

Ports are under scrutiny too, as insurers watch for aggregation of assets and cargo.

New fuels and retrofits bring uncertainty, but also an opportunity to negotiate favorable cover if well documented.

Insurance has shifted from reactive to proactive, shaping contracts and even long-term investment choices.

Insurance as a Strategic Lever Across Maritime Segments

Segment

How Insurance Is Shaping Choices

Adjustment in Practice

Financial Signal

Shipowners

Premium differences between Red Sea routes and safer corridors are guiding chartering and deployment.

Re-routing and building surcharges into contracts.

📉 Higher cost base if exposure can’t be avoided; 📈 improved yield if risk is priced correctly.

Ports & Terminals

Insurers monitor cargo accumulation and resilience measures before setting terms.

Investments in security, yard smoothing, and IT reporting.

Insurance clauses are now a negotiation item, not boilerplate.

Embedding war-risk surcharges and exclusion terms in fixture templates.

📉 More paperwork, but better cost predictability when claims arise.

Financiers

Credit desks weigh insurance availability before green-lighting projects.

Linking loan covenants to cover levels and loss-history data.

📈 Better loan terms for insured assets; 📉 capital withheld if risk is unpriced.

Technology & Data Firms

Underwriters want clean, verifiable data on performance, emissions, and maintenance.

Growth in demand for monitoring software and compliance platforms.

📈 Revenue upside for firms selling verifiable datasets and tracking tools.

Note: Table builds on themes raised at IUMI Singapore and related coverage — focusing on how insurance is actively reshaping strategic choices across maritime segments.