Moody’s says the U.S. ports sector is heading into a tougher 2026 as tariff uncertainty and softer macro growth weigh on import demand and planning. A one-year U.S.–China fee pause offers only temporary relief; most risks resurface when it expires. For shipowners and terminal stakeholders, that means flatter volumes, tighter yields, and more cautious contracting unless policy visibility improves.

Click here for 30 second summary

Simple Summary in 30 Seconds

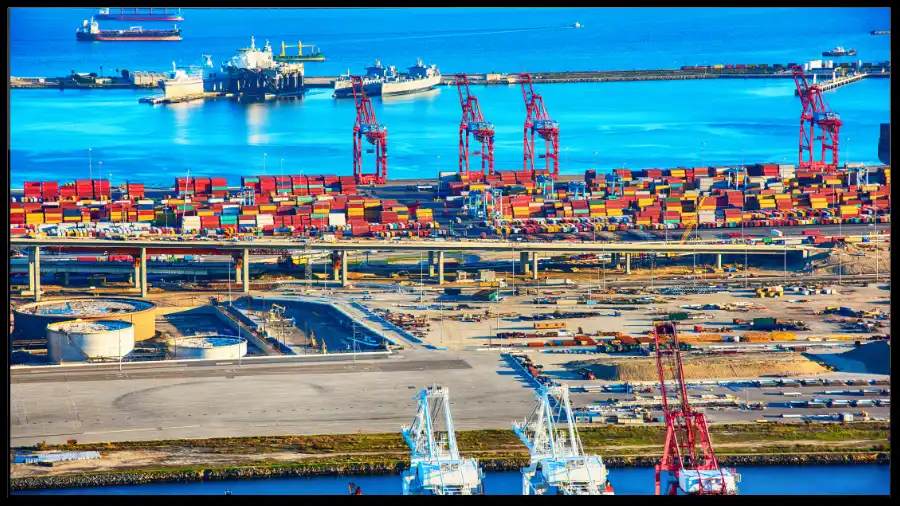

Moody’s sees a tougher 2026 for U.S. ports as tariffs and policy uncertainty weigh on import demand. A temporary fee pause helps in the near term, but planning risk remains. That means softer throughput, tighter pricing power, and more conservative capex until signals improve.

📢 What changed

The sector outlook turns negative for 2026 due to tariff risk, weaker consumer pull, and policy noise that complicates cargo decisions.

💰 Cost and time effect

Lower TEUs reduce operating leverage, incentives and rebates grow, and some projects slow to protect cash and coverage ratios.

📊 Market signal

Spot and contract yields face pressure on Transpac and East/Gulf routes, with cascading risk for mid-size ships if imports soften further.

🔎 Near-term watch

Policy timelines on tariffs, retailer order books for early 2026, and gateway incentive programs aimed at defending volume share.

📌 Bottom line: The fee pause trims friction now, but demand and policy clarity drive 2026 outcomes. Without better visibility, expect tighter margins, heavier discounting, and cautious expansion across major U.S. gateways.

U.S. Ports Face Weaker 2026 on Tariffs and Policy Uncertainty: Industry Impact

Item

Summary

Business Mechanics

Bottom-Line Effect

Moody’s outlook

Moody’s sets the U.S. ports sector 2026 outlook to negative on tariff risk, policy uncertainty, slower U.S. real GDP and moderating consumer spend.

Lower import appetite and planning friction depress container throughput and related fee revenue at gateways.

📉 Softer top line for ports and vendors; 📉 weaker utilization for boxship owners on U.S.-bound lanes.

Volume trajectory into 2026

Industry trackers flag a slower import start to 2026 after a front-loaded 2025; retailers expect a more pronounced slowdown early next year.

Reduced TEUs cut terminal moves, lift per-unit fixed cost absorption, and can trigger cascading to smaller ships.

📉 Charter appetite and freight yields pressured on Transpac and Asia–U.S. intermodal corridors.

Tariffs & fee pause

A one-year U.S.–China pause on port fees and crane/chassis tariffs is in effect, but agencies and analysts frame it as temporary relief.

Some near-term cost friction eases for carriers and terminals; planning risk returns when the pause expires.

📈 Minor cost relief in 2025–26 window; 📉 uncertainty lingers over post-pause policy.

Revenue mix & pricing

With import-led growth softening, ports rely more on non-container revenue lines and negotiated rebates to retain volumes.

Discounting and incentive structures can protect share but compress per-box revenue where competition is high.

📉 Net revenue/TEU at risk in competitive gateways; 📈 stronger negotiating hand for cargo owners.

Credit posture & capex timing

Negative sector outlook implies more cautious leverage and sequencing of capex until traffic trends firm.

Deferrals on big-ticket projects and phased spend help preserve coverage ratios amid slower growth signals.

📉 Slower upgrade cycles for some terminals; 📈 cash preservation over expansion in 2026.

Implications for shipowners

Flatter U.S. import demand narrows lane utilization; carriers may redeploy capacity, accelerate cascading or push longer strings elsewhere.

Contract resets emphasize reliability and landed cost; spot exposure more volatile when macro headlines shift.

📉 Time-charter cover harder to secure at rich levels; 📉 weaker spot where U.S.-bound demand eases.

Notes: Moody’s Ratings published a negative 2026 outlook for U.S. ports; sector press summarized tariff/policy drivers. U.S.–China fee and crane/chassis tariff pauses began Nov 10, 2025 and are time-limited. Retailers’ 2026 import view indicates a softer start to the year. Effects vary by gateway, contract mix and cargo composition.

Traffic pulse into 2026

📦 Import pipeline

Cooling vs 2025

🚚 Landside turn times

Stable to softer

💲 Pricing power

Under pressure

🧾 Incentives/rebates

More prevalent

Throughput risk (next 2–3 quarters)

Contract re-pricing pressure

Capex slow-roll likelihood

Bars are qualitative gauges based on a negative sector outlook, tariff uncertainty and softer import appetite.

Lane sensitivity snapshot

Lane

Pressure now

Transpacific Asia → U.S. West Coast

Front-loaded 2025 fades; spot and contract yields tested.

Asia → U.S. East/Gulf (via Panama)

Cost sensitivity intersects canal tolls and reliability.

U.S. export agri → Asia

Supportive in season, but rate pass-through limited.

Room to win share with reliabilityNon-container revenue cushionsLonger strings can redeploy capacityWeaker import pull lowers TEUsRebates compress per-box revenueCascading pressures mid-size tonnage

Revenue sensitivity mini-calculator

Estimate monthly impact from a change in import volume and pricing.

Estimated monthly revenue change: -$1,532,000

Moody’s negative stance signals a cooler import year and tougher pricing across major U.S. gateways. The fee pause trims some near-term friction, but tariff uncertainty and softer demand keep pressure on yields and contract terms. Ports lean more on incentives and non-container revenue while carriers juggle redeployments and cascading. If policy clarity improves and retail orders stabilize, the soft patch can shorten; if uncertainty lingers, 2026 looks like a year of tighter margins and heightened competition on U.S.-bound lanes.